Everyone’s freaking out about the 50-year mortgage like it’s the end of civilization.

News flash: it’s not good, it’s not bad : it’s a tool.

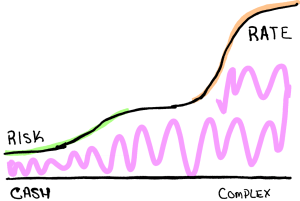

A mortgage is just a wrench in your toolbox to solve one problem: homeownership. Some people buy cash (simple). Others need something more complex (longer term, higher risk). The further you move from cash → the more complex it gets → the higher the rate.

The Cash-to-Complex Continuum

Here’s how the lending world really works, and it’s dead simple.

Picture a line. On the far left, you’ve got cash buyers : zero risk because there’s no bank involved. They’re not borrowing from anybody.

As you move right on this continuum, things get more complex. Most people can’t drop $400K cash on a house, so we need creative solutions. More complex = more risk = higher rates.

That’s it. That’s the entire mortgage industry in one concept.

A 50-year mortgage sits further right on this continuum than a 30-year. More complex, more risk, probably higher rates. But it’s still just a tool to solve the homeownership problem.

This Isn’t Some Crazy New Idea

Before you panic about 50-year mortgages destroying America, let me hit you with some history.

Japan ran 50-year and 100-year mortgages back in the ’90s. They were dealing with hyperinflation and needed ways to get families into homes. It worked.

Here in the U.S., we’ve had:

- One-year ARMs

- Five-year terms

- 40-year mortgages

- Interest-only loans (that’s infinite : you just pay interest forever)

So a 50-year mortgage? It’s not some apocalyptic financial weapon. It’s another option in the toolkit.

Why the 50-Year Makes Sense (Sometimes)

Let’s get real about who this actually helps.

The 25-year-old buyer: They’re not staying in that starter home forever. Most people refinance every 5-6 years anyway. A 50-year mortgage gets them in the door to start building equity instead of throwing money at rent.

The market reality: The average age of a first-time homebuyer is now 40. Forty! If a 50-year mortgage brings that number down and gets people into homeownership earlier, that’s a win.

The payment difference: On a $400,000 loan, you might save $250-400 per month with a 50-year term. That’s groceries, car payments, or emergency fund money.

Stop the Financial High Horse

We need to talk about our collective financial decision-making before we trash 50-year mortgages.

We lease cars we can’t afford. We upgrade phones every two years. We DoorDash dinner when our bank account is crying. We rack up credit card debt at 24% interest.

But suddenly, a 50-year mortgage makes us “financially irresponsible”?

Come on.

If you’re going to judge financial tools, at least be consistent. Most Americans are terrible with money across the board. A mortgage tool that gets someone into homeownership isn’t the problem.

When It Works (And When It Doesn’t)

It works when:

- You’re young and plan to refinance or move within 10 years

- You need lower payments to qualify for the loan

- You’re in a high-cost area where it’s the only way in

- You understand the trade-offs and choose them anyway

It’s a trap when:

- You think you’re getting a “deal”

- You plan to keep the same mortgage for 50 years

- You ignore the total interest cost

- You use it to buy more house than you can actually afford

The Real Enemy Isn’t 50-Year Mortgages

Want to know what’s really making homes unaffordable?

- Insurance costs going through the roof

- Property taxes that increase every year

- Construction costs and labor shortages

- Zoning laws that prevent affordable housing

- Investment firms buying up single-family homes

A 50-year mortgage is like blaming the Band-Aid for the cut. It’s treating a symptom, not the disease.

But sometimes you need the Band-Aid while you figure out the bigger problem.

Your Job as a Broker

Here’s what matters: your client’s situation, not your opinion about mortgage terms.

Someone walks into your office. They make decent money but can’t qualify for a 30-year mortgage on the home they want in their area. You’ve got options:

- Tell them they can’t afford homeownership (they rent forever)

- Push them into a smaller, cheaper area (they commute two hours daily)

- Show them a 50-year option (they get the house, start building equity)

Which one actually solves their problem?

Your job isn’t to be the financial morality police. It’s to present options and let educated adults make decisions about their own lives.

The Bottom Line

A 50-year mortgage is a tool on the cash-to-complex continuum. Like any tool, it can build something useful or tear something down, depending on how you use it.

The real question isn’t “Is it good or bad?”

It’s “Does it solve this person’s problem today?”

Maybe your client is 28, planning to start a family, and knows they’ll move to a bigger house in seven years. The 50-year mortgage gets them out of rent and into equity-building mode right now.

Maybe your client is 45, buying their forever home, and plans to pay extra toward principal anyway. The 50-year gives them flexibility without forcing them into higher payments.

Maybe your client is 35, divorced, starting over financially, and needs the lowest possible payment to rebuild. The 50-year mortgage gives them stability and a fresh start.

Every situation is different. Every client has different goals, timelines, and risk tolerance.

Be Open-Minded

Stop judging the toolbox and start finding the right tool.

Your clients don’t need your moral judgment about their mortgage choice. They need your expertise to understand their options and make informed decisions.

Present the facts. Explain the trade-offs. Let them decide what works for their life.

That’s what good brokers do.

That’s what professional service looks like.

And that’s how you build a business that actually helps people instead of just lecturing them about what they should want.

The 50-year mortgage isn’t the end of responsible lending. It’s another option for people who need it.

Use it wisely, explain it clearly, and remember : you’re here to solve problems, not create more of them.